Why cash-basis accounting fails PE diligence

If there is one financial gap that kills more PI law firm deals than any other, it is cash-basis accounting. Not because the firm’s economics are bad — usually they are quite strong. But because cash-basis financials cannot prove it in the language investors speak.

How contingency-fee economics distort cash-basis reporting

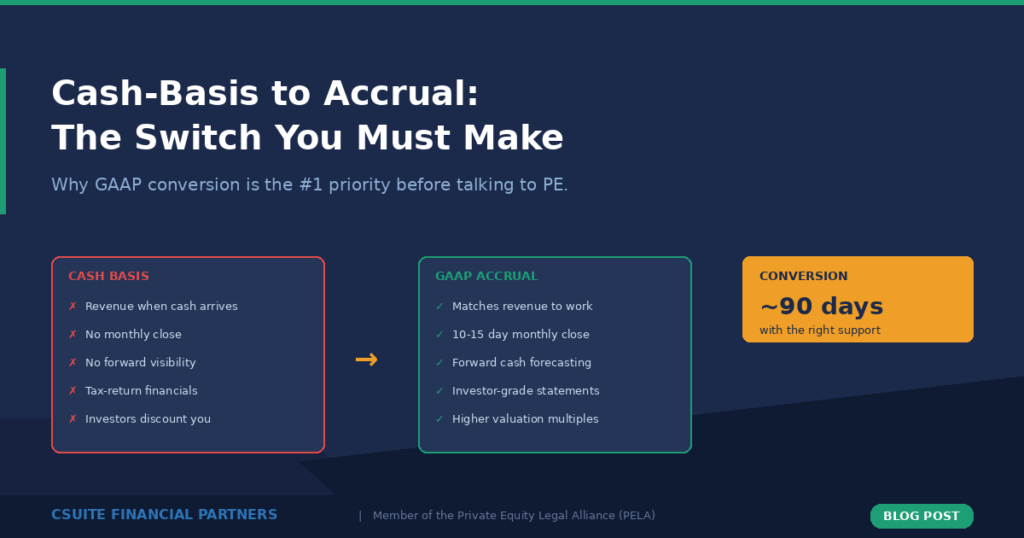

Private equity expects GAAP-compliant accrual reporting. That is non-negotiable. For personal injury firms, the gap between cash-basis and accrual is wider than in most industries because of how contingency-fee economics work.

Under cash-basis accounting, revenue is recognized when cash is received — typically when a settlement check clears. Expenses are recognized when paid. This is simple and intuitive, which is why most founder-led firms use it. But it creates a distorted picture of the firm’s actual economic performance.

Consider a firm that signs one hundred cases in January. They spend heavily on marketing and staff throughout the year, and starts collecting settlements in September. Under cash basis, the first eight months show massive losses. Months nine through twelve show a windfall. The annual number might look fine, but the monthly and quarterly statements are meaningless for forecasting or performance management.

Under accrual accounting, expenses are recognized as incurred — even for ongoing cases — but revenue cannot be recognized until the case is resolved and the fee is earned. This creates a different timing challenge, but it produces financial statements that accurately match economic activity to the periods in which it occurs. Investors can see the real cost structure, understand the relationship between marketing spend and case acquisition, and model forward cash flows with confidence.

The conversion from cash to accrual is not trivial. Here is what it involves.

Step one: rebuilding the chart of accounts

The first step is rebuilding the chart of accounts. Most PI firms have a chart of accounts designed for tax preparation, not financial management. It needs to be restructured to provide the granularity investors expect — marketing spend broken out by channel, case costs separated from overhead, attorney compensation distinguished from staff compensation, and trust account activity clearly segregated.

Step two: implementing monthly close procedures

The second step is implementing monthly close procedures. The target is closing the books within ten to fifteen business days after month-end. This means all transactions are recorded, all accounts are reconciled, all accruals are posted, and financial statements are produced on a consistent timeline. For firms that have historically done an annual close with their tax accountant, this is a significant operational change.

Step three: trust account reconciliation

Trust account reconciliation is the third critical component. PI firms handle client funds in trust, and these accounts must be reconciled regularly and kept separate from operating accounts. Investors and their lenders will scrutinize trust account management closely because mishandling client funds is both an ethical violation and a financial risk.

Step four: documenting revenue recognition policy

Revenue recognition policy must be documented. For contingency-fee firms, revenue is generally recognized when the case is resolved and the fee is determinable and collectible. The policy needs to address how cases at various stages are treated. For example, how fee reductions or write-offs are handled, and how referral fees and co-counsel arrangements affect recognition.

Producing monthly financial statements

Once these foundational elements are in place, the firm produces monthly financial statements: income statement, balance sheet, and cash flow statement. These statements should include variance analysis against budget and prior periods, giving management and future investors visibility into trends and performance drivers.

How CSuite executes the conversion

The timeline for this conversion is typically ninety days with dedicated support. However, the real value comes from running on the new system for several quarters before going to market. Twelve months of clean, consistent accrual-based financials tells a much stronger story than three months of recently converted statements.

At CSuite Financial Partners, the cash-to-accrual conversion is often our first engagement with a PI firm. We bring in interim resources to execute the conversion because we do not expect the existing team to know how to do this — most have never worked in an accrual environment. The goal is to build the system and train the team so they can sustain it going forward.

The cost of this conversion is modest relative to the deal value at stake. The cost of avoiding it appears in lower multiples, wider earn‑outs, and buyer‑favored terms driven by mistrust in the numbers.

If your firm is on cash basis and you are thinking about a sale in the next one to three years, start the conversion now. It is the single highest-return investment you can make in your firm’s transaction readiness.