Every private equity buyer will perform a Quality of Earnings analysis before closing a deal with your law firm. It is their way of verifying whether your profits are real, recurring, and sustainable. If you have never been through a transaction before, understanding what a QoE examines — and preparing for it — can be the difference between a strong deal and a disappointing one.

What a quality of earnings report examines

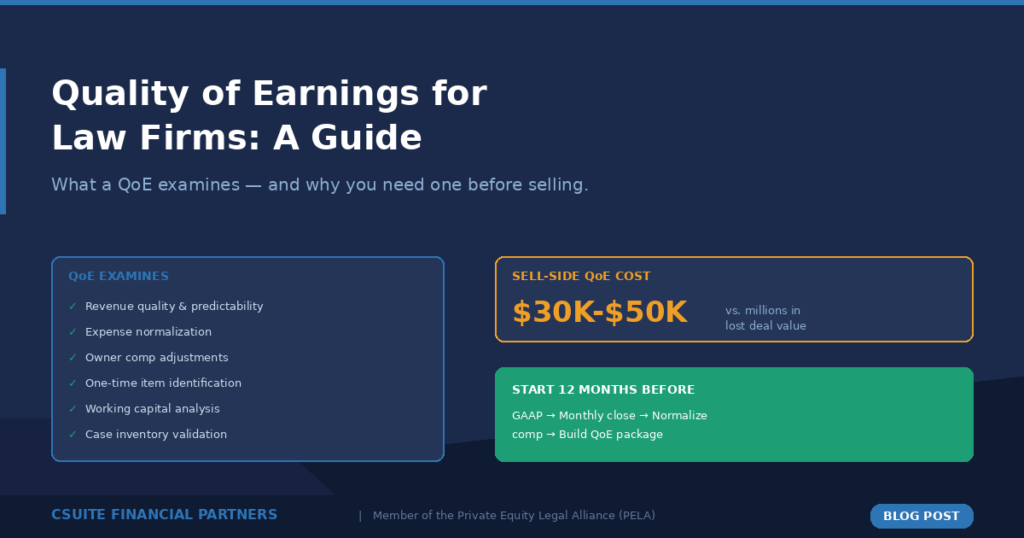

A Quality of Earnings report is a financial diligence analysis that goes deeper than a standard audit. While an audit confirms that financial statements are prepared in accordance with accounting standards, a QoE examines whether the earnings those statements report are actually reliable indicators of the firm’s go-forward profitability.

Revenue quality and case inventory

For a PI law firm, the QoE will focus on several specific areas. Revenue quality is the first. The analyst will examine whether revenue is recurring and predictable or lumpy and dependent on a few large settlements. They will look at your case inventory to understand the pipeline — how many cases are open, at what stages, with what expected values. They will assess your historical realization rate: what percentage of estimated fees actually gets collected.

Expense normalization and owner compensation

Expense normalization is the second major area. This is where most founder-led firms get surprised. The QoE will identify every expense that would not exist in a post-transaction environment and strip it out. Personal expenses flowing through the business — vehicles, travel, meals, family cell phone plans — will be removed. Family members on payroll who may not continue after the deal will be flagged. Above-market rent on properties owned by the founder will be adjusted to fair market value.

Owner compensation is the single largest normalization in most PI firm deals. Before a transaction, the founder takes home the firm’s entire profit. After, they draw a market-rate salary. The QoE will normalize compensation to what it would cost to hire a managing partner or CEO at market rates, and the difference becomes part of the EBITDA base.

One-time items and working capital analysis

One-time and non-recurring items will be identified and adjusted. A large marketing pilot that ran for one quarter, a legal settlement the firm paid, a one-time office build-out — these get stripped from the normalized earnings because they are not expected to repeat.

Working capital analysis is another critical component. The QoE will examine your cash conversion cycle — how long it takes from incurring costs on a case to collecting the settlement fee. For PI firms, this cycle can be nine to twelve months or longer. The analyst will assess whether the business has sufficient working capital to sustain operations post-close and will establish a working capital target that becomes part of the purchase agreement.

Why a sell-side QoE is worth the investment

Smart sellers do not wait for the buyer to perform a QoE. They commission their own sell-side Quality of Earnings ahead of time. The cost is typically thirty to fifty thousand dollars — a fraction of the deal value — but it provides enormous benefits. A sell-side QoE gives you a professionalized set of financials that investors trust. It identifies issues before they are uncovered during due diligence, when they have maximum negative impact on valuation. It accelerates the deal timeline because the buyer’s diligence team can rely on your report as a starting point.

How CSuite prepares firms for QoE diligence

At CSuite Financial Partners, QoE preparation is one of our core services for PI firms. We work alongside firms to clean up financials, document normalizations, and build the supporting schedules before the sell-side QoE engagement begins. The firms we work with go into diligence with confidence because there are no surprises waiting to be uncovered.

The ideal timeline for QoE preparation

The ideal timeline is twelve months before going to market. That gives you time to convert to accrual accounting if needed, implement monthly close procedures, normalize compensation, and build at least two to three quarters of clean, consistent financial reporting. It is possible to compress that timeline, but the more history you have on institutional-grade financials, the stronger your position.

If you are thinking about a transaction in the next one to three years, start the QoE preparation now. The cost of preparation is small. The cost of being unprepared is measured in multiples of EBITDA you will never recover.